New CUScorecard data shows a more disciplined industry heading into 2026—but widening performance gaps and early credit pressure could define what comes next. Insight from CU Scorecard data (BlastPoint)

U.S. credit unions closed out 2025 in a stronger position than many expected. Growth held steady, margins improved in the fourth quarter, and balance sheets showed signs of stabilization after several years of rate-driven disruption.

But for the first time in years, the industry is shrinking.

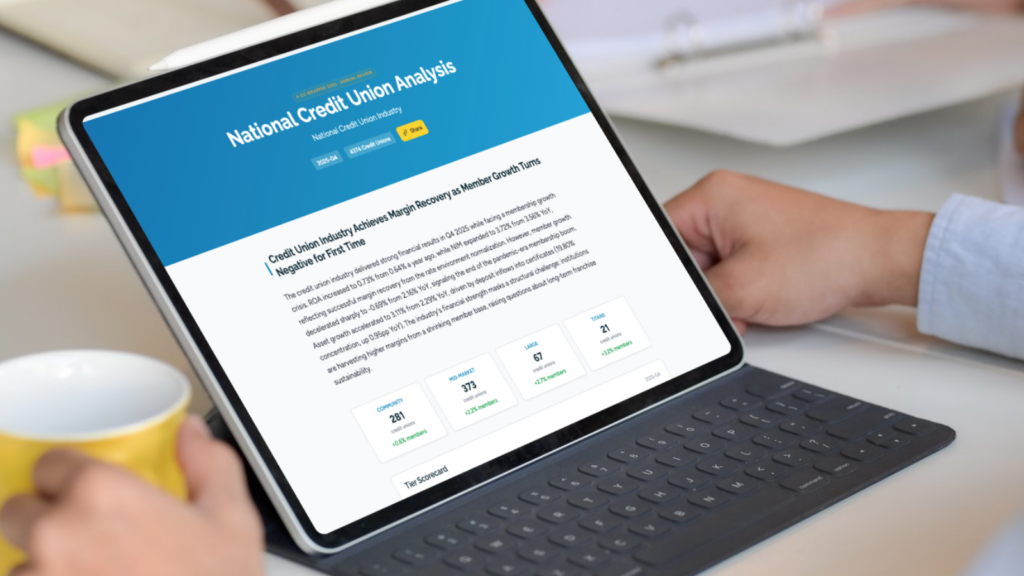

Updated CUScorecard data shows member growth fell to -0.69% year-over-year in Q4, down from +2.16% a year ago, marking a clear end to the pandemic-era expansion cycle. At the same time, ROA rose to 0.73% and net interest margin expanded to 3.72%, signaling a successful recovery in earnings.

The result is a striking dynamic:

Credit Unions are becoming more profitable while serving fewer members.

The Headline Growth Number Is Hiding the Real Story

At first glance, industry-level member growth appears modestly positive.

But that number is misleading.

A handful of large institutions are masking a broad-based contraction across the industry. On an equal-weighted basis, member growth is -0.69%, and 83% of credit unions are losing members.

The divide is stark:

- Credit unions above $500M in assets are growing

- Credit unions below $500M are shrinking

The spread between small institutions (-1.6%) and the largest (+3.2%) is now 4.8 percentage points and widening.

This is no longer just a growth slowdown. It’s a scale-driven separation.

Profitability Has Recovered But It’s a Tailwind, Not a Strategy

Margins improved significantly in 2025, with NIM reaching 3.72%, driven by:

- Faster repricing of variable-rate loans

- Slower adjustment of deposit costs

But this is largely a rate cycle windfall, not an operational achievement.

Credit unions are benefiting from macro conditions they did not create and that will not last indefinitely.

The uncomfortable reality:

Institutions are harvesting higher margins from a shrinking member base.

Those that used this window to invest in member growth and digital capabilities are positioning for the future. Those that did not may be exposed when rates normalize.

The Membership Model Is Breaking Down

Three structural forces are driving the decline in membership:

- Fintech competition: Digital-first players like SoFi and Chime are capturing younger demographics

- Indirect lending pullback: Now at 7.78% of portfolios, removing a key acquisition channel

- Demographic pressure: The average credit union member is aging, with no replacement pipeline at scale

The result is a system that is no longer naturally replenishing its member base.

For many institutions, this is the most important shift in the data.

Growth Is Being Driven by Deposits, Not Demand

Balance sheet growth accelerated in Q4, with assets growing 3.11% year-over-year.

But the composition of that growth raises questions.

Deposit inflows, particularly into certificates, now 19.80% of balances are driving expansion. Meanwhile, loan growth remains subdued at 0.52%, reflecting constrained demand in a high-rate environment.

Looking ahead, certificates represent a key pressure point.

As 2024–2025 vintages mature through 2026, credit unions will face a wave of member decision moments:

- Reprice and retain deposits at higher cost

- Or risk outflows if engagement is weak

This is shaping up to be one of the industry’s most immediate tests.

Credit Remains Stable….for Now

Credit quality has held up, with delinquency at 0.90% and strong capital levels (13.68% net worth ratio).

But forward indicators are shifting.

Tariff-driven inflation, particularly in autos, could increase prices by 10–15%, reducing loan demand while increasing borrower stress. Combined with broader economic uncertainty, this creates potential pressure on both origination volume and credit performance in the second half of 2026.

The Real Divide Is Scale and It Will Define 2026

What looks like a profitability divide is increasingly a scale economics divide.

Smaller credit unions, 83% of the industry by count, are losing members while facing the same fixed costs for digital, compliance, and infrastructure as larger peers. With growth no longer offsetting those pressures, consolidation is likely to accelerate.

Heading into 2026, the industry is becoming more disciplined but more fragile: margins are strong but cyclical, growth is uneven, and membership is declining.

The institutions that outperform won’t just manage margin. They’ll rebuild member acquisition, compete for digital-first consumers, and use data to actively manage retention and risk.

Explore the Full 2025 Analysis

The CUScorecard has been updated with Q4 data and a full 2025 year-in-review, including national, state, and peer-level trends.

peer-level trends.

Explore the latest insights here:

👉 https://cuscorecard.blastpoint.com/

About CU Scorecard

CU Scorecard is a free, interactive benchmarking tool developed by BlastPoint to help credit unions understand how they compare across national and state-level industry trends. Every insight is backed by official NCUA data from more than 4,800 federally insured credit unions, combined with continuously updated industry signals. CU Scorecard highlights patterns in financial performance, digital presence, and brand reputation, giving credit union leaders actionable context.

Access the full CU Scorecard national and state-level analyses here:

👉 https://cuscorecard.blastpoint.com